General

Publications & Data

Join the conversation

Social Links

Social Links

This report summarises the key domestic and international data releases over the past week, including stronger-than-expected first-quarter GDP growth in SA and a mixed start to the second quarter for mining and manufacturing. Internationally, we cover the ECB’s first interest-rate hike in nearly three years, accelerating US inflation and the latest inflation developments in China as policymakers continue to grapple with the economic consequences of higher energy prices and heightened geopolitical uncertainty.

The full BER Weekly Review also examines the latest developments in the Middle East, where military escalation and peace negotiations are unfolding simultaneously, the implications for inflation and interest rates, and Natasha Marrian’s analysis of the ANC’s shifting approach to the immigration debate ahead of November’s local government election. The full Weekly is available to BER Essential Insights subscribers (sign up here for only R210/month) and Premium Insights clients.

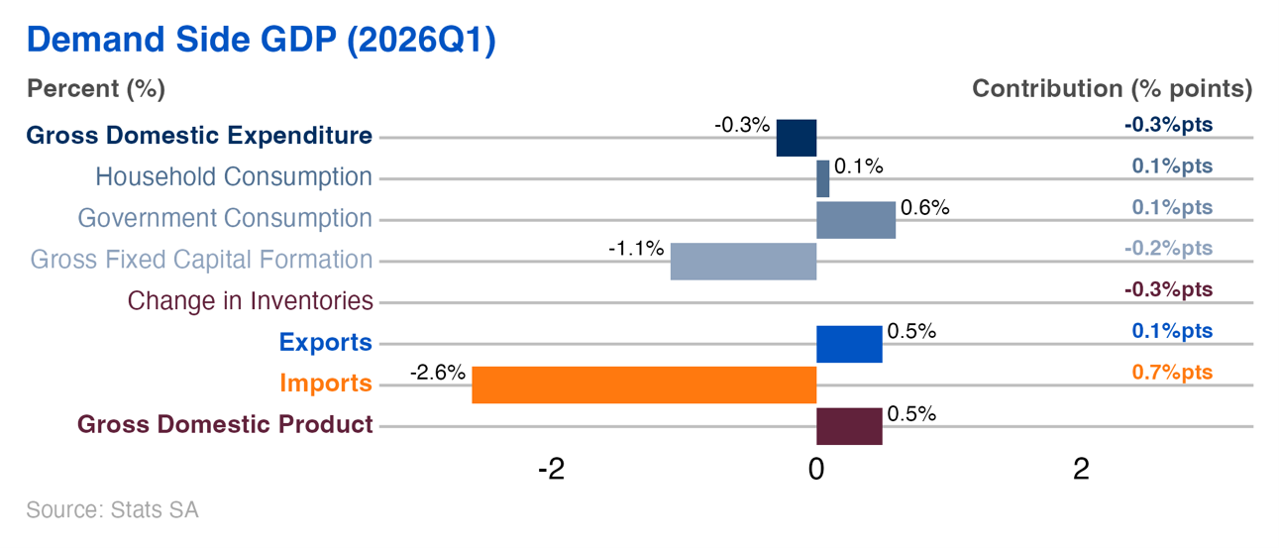

The SA economy registered its sixth consecutive quarter of quarterly growth, booking a better-than-expected 0.5% expansion in Q1. Annually, real GDP growth registered 2.1%. This follows an (unrevised) 0.4% expansion in 2025Q4. However, while the headline GDP outcome was encouraging, the composition of growth was less so.

On the expenditure side, consumer spending decelerated markedly, although, given the sheer size of consumer spending in the economy (64% of GDP), the 0.1% q-o-q expansion still added 0.1% pts, the slowest since 2024Q1, though the 3.4% annual print was largely in line with our forecasted 3.5% expansion. More concerning was gross fixed capital formation, which contracted by 0.1% q-o-q after two quarters of growth, with private-sector capex almost fully erasing the gains booked in 2025. The main support for GDP growth came from the external sector rather than domestic demand: exports edged up by 0.5% q-o-q, while imports contracted sharply by 2.6%. The composition of growth, therefore, reinforces the view that underlying momentum is less impressive than the headline figure suggests.

Higher exports and lower imports also led to the current account surplus widening to 2.4% of GDP in 2026Q1, up from 0.6% in Q4, and the largest since 2022.

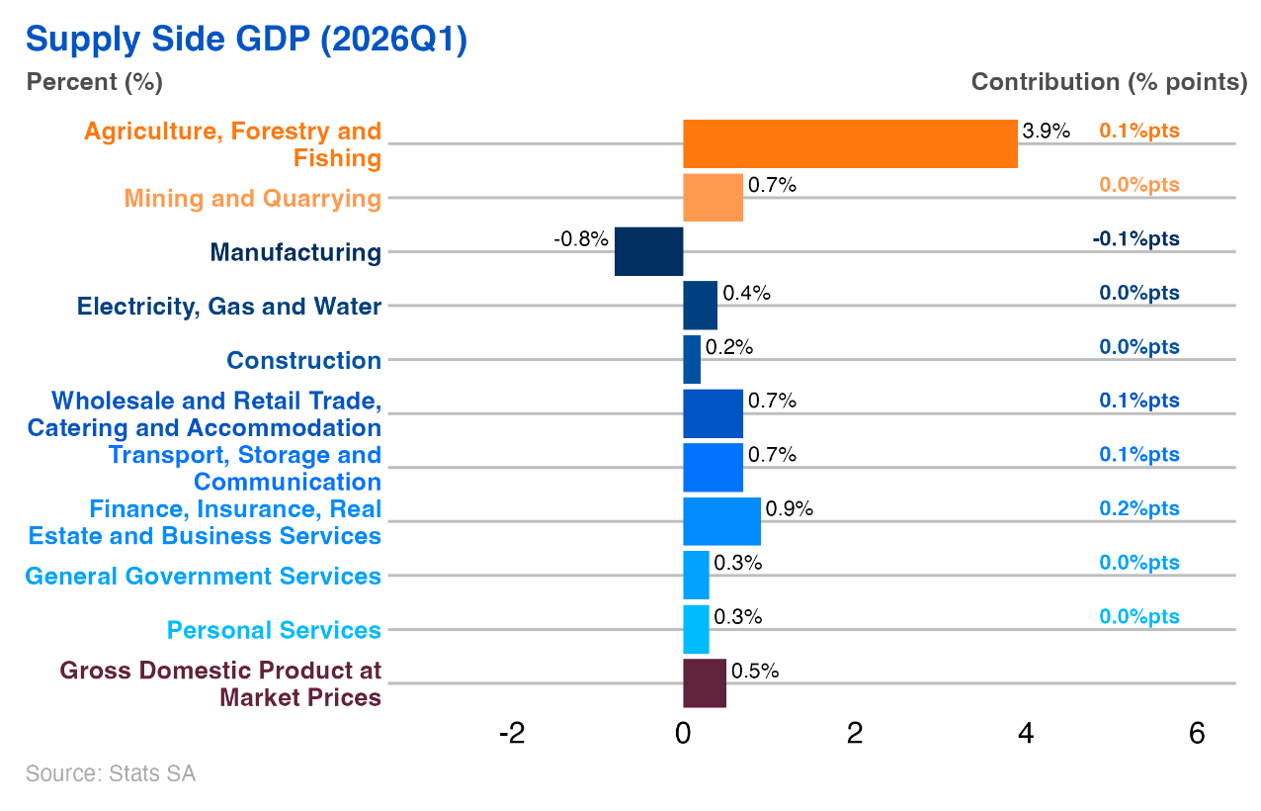

From the production side, the agriculture sector posted strong gains, while the finance sector, the largest sector of the economy at 21%, contributed the most. The manufacturing sector was the only drag, a decline already foreshadowed by the monthly production data. The quarter again highlighted the widening divergence between the service economy and the goods-producing sectors. While nine of ten sectors expanded, the secondary sector remains a persistent constraint on growth.

Not all the week's scorecards disappointed. Impumelelo’s latest reform tracker points to continued, if uneven, progress on the government's structural reform agenda. While these gains are unlikely to offset near-term global headwinds, they do suggest that the economy is better placed to weather external shocks than it was a few years ago.

Mining production increased by 8.2% y-o-y in April, with the largest contributors being PGMs (up 36.5% y-o-y), manganese ore (up 19% y-o-y), and chromium ore (up 17.5% y-o-y). Coal production, meanwhile, contracted on an annual basis (down -5.8% y-o-y). Positive for Q2 GDP, output rose by 3.3% m-o-m. Mining production is up by 6.1% so far this year, likely aided by sustained higher commodity prices. It is no surprise then that mineral sales at current prices also saw robust annual growth of 30.3% in April.

On the other hand, manufacturing production decreased by 2.9% y-o-y. The largest detractors were basic iron and steel, non-ferrous metal products, metal products and machinery (-6%, subtracting 1.4 %pts), wood and wood products, paper, publishing and printing (-10% y-o-y, subtracting 1 %pt), and motor vehicles, parts and accessories (-11% y-o-y, subtracting -0.9 %pts). Unlike mining, the factory sector had a tough start to Q2, with production decreasing by 2.7% m-o-m after 1.2% m-o-m growth in March.

On Thursday, the ECB raised its policy deposit rate by 25bps, from 2.15% to 2.4%, marking its first rate hike in nearly three years. This makes the ECB the first developed-economy central bank to move in response to elevated energy prices amid the ongoing Iran conflict, reaffirming its commitment to keeping inflation anchored at its 2% target. ECB president Christine Lagarde noted that, as the outlook remains uncertain, the decision to hike is supported by a range of scenarios that map out how the energy shock might evolve and the subsequent impact on the EZ medium-term outlook. However, she emphasised that the bank has not yet committed to an interest rate path, as this depends on the duration of the energy shock and the potential extent of its second-round effects.

Indeed, baseline staff macroeconomic projections presented upward revisions to headline inflation in 2026 and 2027, reflecting a higher path for energy prices and the spillovers into food and services inflation. Meanwhile, growth expectations were downwardly adjusted to reflect a reduction in purchasing power and confidence.

Across the Atlantic, price gauges continued their ascent as energy prices quickened for a third consecutive month. Annual headline consumer inflation accelerated to 4.2% in May, up from 3.8% in April. On a monthly basis, headline CPI rose by 0.5%, a touch lower than April’s 0.6%. Still, a 3.9% m-o-m rise in the price of energy-related goods contributed to more than 60% of the rise in the monthly CPI. Core inflation, which excludes volatile food and energy prices, reached 2.9% y-o-y in May, its highest level since September 2025.

Factory gate inflation (PPI) rose by an above consensus 1.1% y-o-y in May, unchanged from a downwardly revised 1.1% rise in the prior month. The upside surprise was mainly led by a faster pace of price growth in goods (up 2.8% in May, from 1.9% in April). According to the Bureau of Labour Statistics, this marks the largest increase on record for the final demand good index (series begins in 2009), with over half of the rise attributed to a 23.4% m-o-m acceleration in gasoline prices.

In China, prices in the economy are showing some sustained but uneven recovery from deflationary pressures. Consumer inflation held steady at a below consensus 1.2% y-o-y in May, as firmer transport price increases driven by elevated energy costs were offset by a deceleration in food prices, owing to persistently weak pork prices. On the other hand, producer price inflation jumped from 2.8% y-o-y in April to 3.9% y-o-y in May. This marked the fastest pace of price growth in nearly four years, driven by a rise in raw material costs and energy prices, aided further by Beijing’s effort to curb overcapacity in the production sector. Higher production material costs, particularly in mining and raw materials, drove the acceleration in factory gate prices, even as consumer goods prices remained mildly deflationary.

Friday, 12 Jun 2026