General

Publications & Data

Join the conversation

Social Links

Social Links

This report covers the key data releases domestically and internationally over the past week and updates on crucial structural reform initiatives. It is a shortened version of the more comprehensive BER Weekly Review (Enhanced version), which includes a detailed discussion on the main economic events and developments over the past week, a summary of upcoming data (the week ahead) and the BER’s forecast for key economic indicators. The full Weekly is only available to BER Essential Insights subscribers (sign up here – it’s only R210/month) and BER Premium Insights clients.

The seasonally adjusted Absa PMI declined by 1.4 index points to 49.5 in August, slipping back into contractionary terrain. This partially reversed July’s 2.3-point improvement, which had briefly lifted the index above the neutral 50-point mark for the first time in nine months. Activity in the sector remained subdued, with both domestic and export demand continuing to disappoint. That said, it is worth noting that the average PMI for Q3 thus far (with September data still outstanding) is tracking 4.8 points above the Q2 average, pointing to some underlying improvement. A further positive came from a decrease in the purchasing price index, suggesting some relief on the input cost front.

Similarly, the S&P Global South Africa PMI edged down by a fractional 0.2 index points to 50.1 in August. This marked the fourth consecutive month of expansion, albeit just above the neutral threshold. While new orders and output continued to improve, overall sales performance remained weak, particularly in export markets. Another area of concern was employment, which fell back after two consecutive months of growth. On the upside, input cost inflation moderated, registering the slowest rate of increase in ten months.

The RMB/BER BCI declined marginally by one point to 39 in the third quarter of 2025, following a five-point drop in the second quarter. This places the index three points below its long-term average of 42. The underlying survey results suggest an economy that continues to muddle through, with several activity and demand indicators hovering around their 20-year average levels. Yet, overall, the current level of confidence remains too low to support the kind of investment activity needed to lift South Africa’s potential growth and job creation prospects over the medium term.

Premium Insights Clients can now access our proprietary survey data directly on the BER Data Playground. The data will be released on the Playground in the afternoon of each survey release. Access the Data Playground. (Ensure you are logged in to unlock access to the survey data, which will be updated with subsequent BER survey releases - view the BER Release Calendar).

NAAMSA’s new vehicle sales rose nicely in August, with overall vehicle sales increasing to 51 880, its highest level since October 2019. This represents an 18.7% y-o-y increase. Domestic sales performed particularly well, possibly lifted further by the 25 bps interest rate cut announced at the end of July. Passenger vehicle sales rose by a notable 22.5% y-o-y, signalling robust consumer demand. Export sales also recorded growth, albeit at a more moderate pace of 6.2% y-o-y.

Electricity production declined by 2.3% y-o-y in July 2025. That said, on a year-to-date basis, there has been a modest improvement in output, with production up by 0.7% compared to the same period last year. Electricity consumption followed a similar pattern. Usage was down by 4.5% y-o-y in July 2025, and for the year thus far, consumption is 2.3% lower than during the same period in 2024.

Roy Havemann

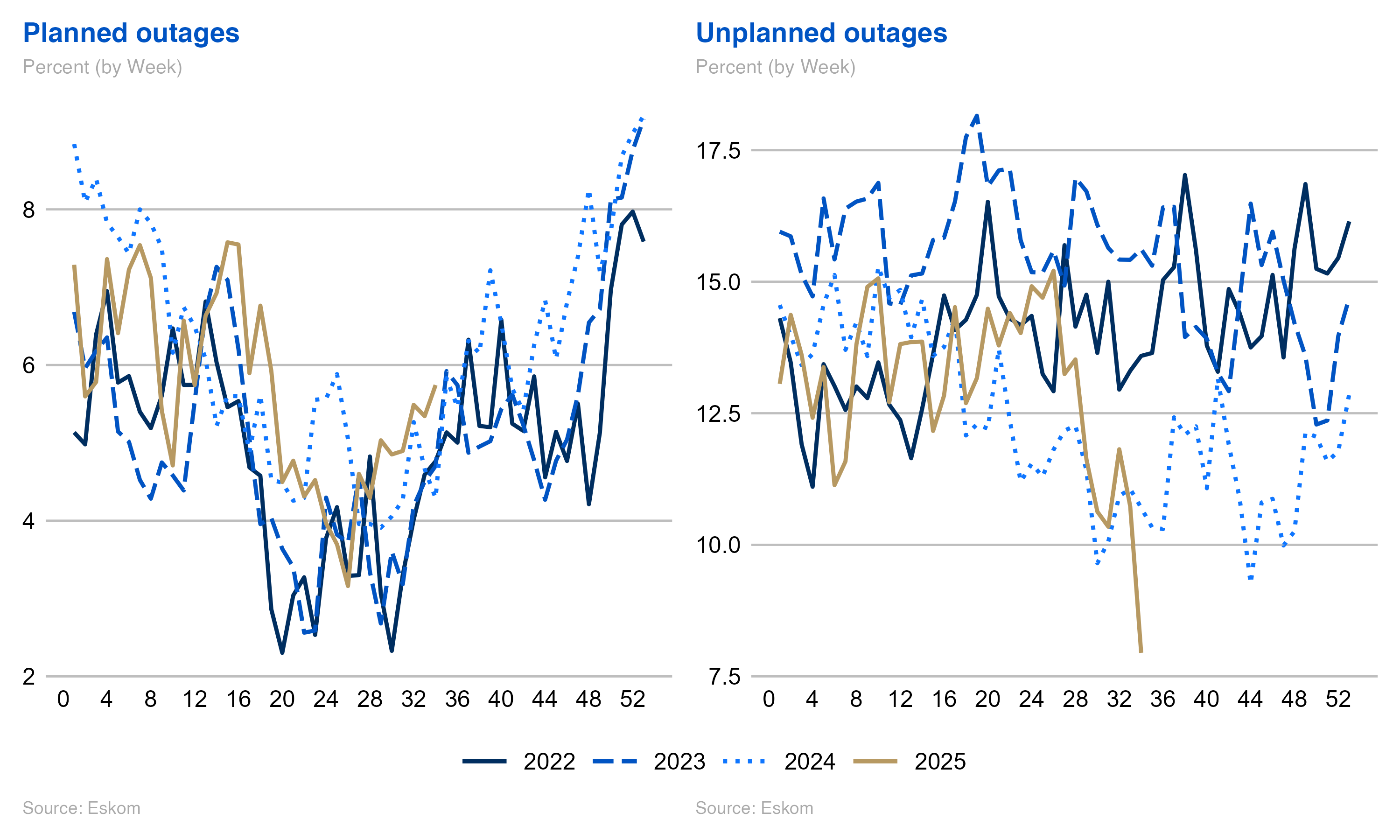

On the reform front, a positive development this week was the outcome of earlier reform, with Eskom’s energy availability factor (EAF) improving markedly. The improvement is largely due to lower unplanned outages, a sign that its maintenance plan might be paying off.

.png)

China’s NBS manufacturing PMI rose marginally to 49.4 in August, remaining in contraction for the fifth consecutive month. Stronger output growth and a slight uptick in new orders underpinned the improvement. Additionally, the non-manufacturing PMI edged up by 0.2 points to 50.3. Taken together, these results suggest a mild acceleration in growth momentum.

The RatingDog China Manufacturing PMI (formerly CAIXIN) rose to 50.5 (vs 49.5 in July) amid a rebound in domestic demand. However, export orders remained slightly weaker. The services PMI rose to 53.0, the best level since May 2024.

The unemployment rate fell back to a record low of 6.2% in July, down from 6.3% in June. The labour market is expected to remain robust, as the latest European Commission survey results indicate increased employment expectations.

Factory output growth expanded at its fastest pace in more than three and a half years as the HCOB Manufacturing PMI rose above the no-change threshold to 50.7 in August (vs. 49.8). The improvement was underpinned by an increase in new domestic orders.

Conversely, the Services PMI slowed to 50.5 in August (vs. 51.5) amid a sharp fall in exports, while both selling and input prices accelerated.

The flash headline consumer inflation rate rose to 2.1% y-o-y in August, slightly above market expectations of 2%. Core inflation held steady at 2.3%, the lowest level since January 2022. Producer price inflation, on the other hand, eased to 0.2% y-o-y from 0.6% in July. Retail trade, however, weakened at the start of Q3, with July sales down 0.5% m/m, the steepest fall in two years.

In August, the ISM Manufacturing PMI edged up to 48.7 (vs. 48), marking the sixth consecutive month of contraction. A rebound in new orders and new export orders drove the increase. Prices remained elevated but increased at a slower pace (63.7 vs. 64.8). Meanwhile, the S&P Global Manufacturing PMI rose to 53.0 (vs. 49.8), the highest reading in three years. This was driven by production growing at its fastest pace since May 2022, supported by increased new orders.

The S&P Global US Services PMI edged down to 54.5 (vs. 55.7). New business expanded at its second-strongest rate this year, driven mainly by rising demand in financial services, which helped counter slower growth in consumer services impacted by tariffs. Conversely, the ISM Services PMI expanded at a faster pace, rising to 52 (vs. 51). Commentary highlighted ongoing tariff-related pressures, with some businesses accelerating activity and imports to pre-empt further price increases ahead of the holiday season.

The S&P Global UK Services PMI for August rose sharply to 54.2 (vs. 51.8), the fastest expansion in over a year amid a rebound in new business. However, firms continued to face higher costs, raising prices at the fastest pace since April, and employment fell for an eleventh consecutive month.

Meanwhile, the manufacturing print fell to 47.0 (vs. 48), its eleventh month in contraction due to a drop in domestic and export orders. Employment declined for ten straight months, while supply chain disruptions and rising input costs pushed input price inflation to its highest since May, with some pressures passed on to customers.

Editor: Lisette IJssel de Schepper

Tel: +27 (0)21 808 9777

Email: lisette@sun.ac.za

Please refer to the glossary on the BER website for explanations of technical terms.

Friday, 05 Sep 2025