General

Publications & Data

Join the conversation

Social Links

Social Links

Outside of the concerns about a recent streak of foodborne illnesses in SA, there was some positive news to share on the domestic front this week. The rand strengthened following welcome news late last Friday that the credit rating agency S&P Global had upgraded SA’s rating outlook from stable to positive. This decision was driven by plans for accelerated economic reforms under the Government of National Unity (GNU) and the expectation of increased private sector investment. The GNU has helped alleviate some of the significant political risks weighing on the country’s credit rating, but faster economic growth is needed before we see credit rating upgrades. Still, the improved outlook likely contributed to a slight drop in bond yields, which had declined by 16 basis points (bps) by the end of Thursday.

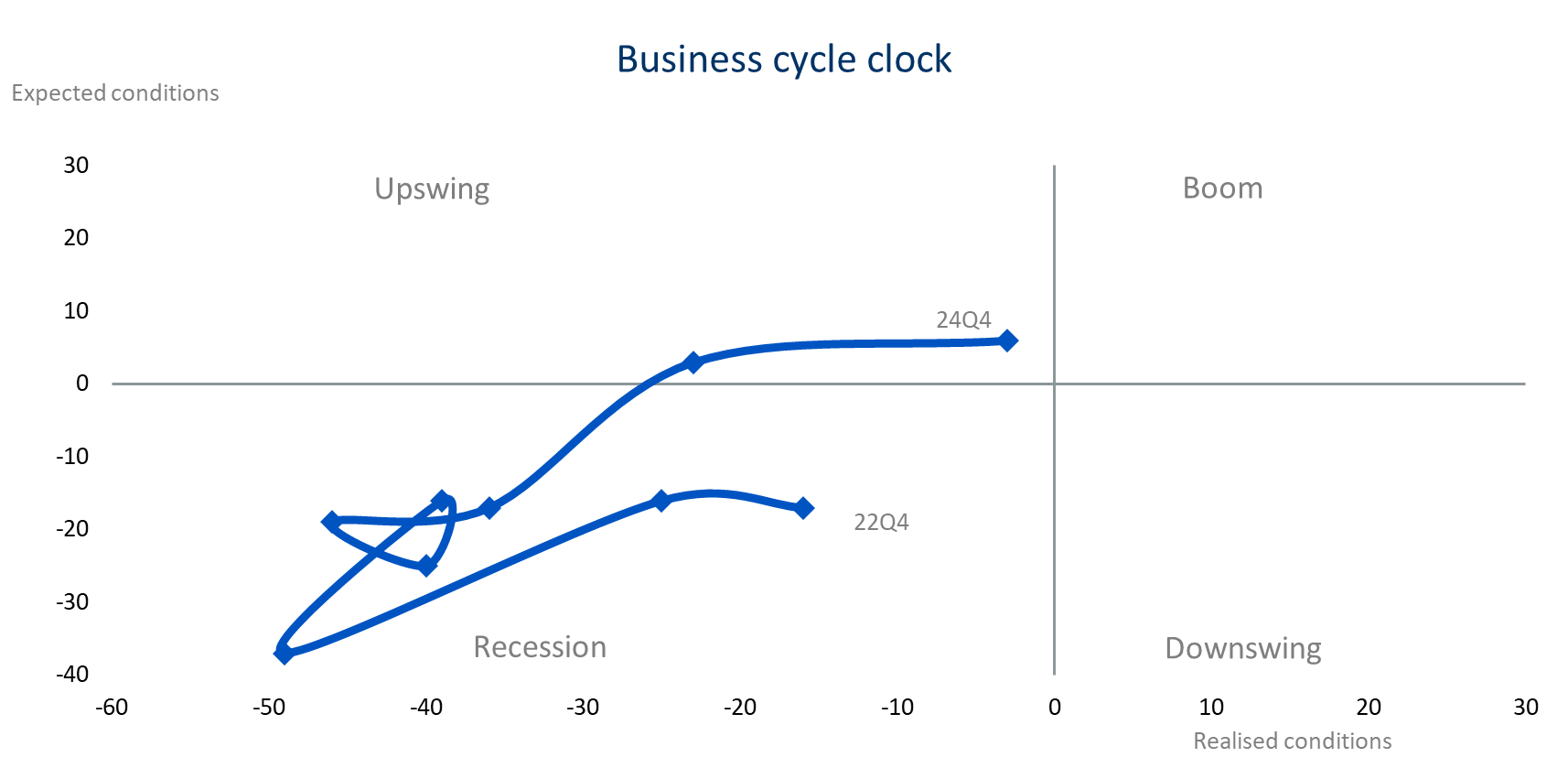

On Tuesday, further optimism came when data from Stats SA showed that annual consumer inflation moderated to 2.8% in October, the lowest level in nearly four years. This was followed by the release of the Q4 RMB/BER Business Confidence Index (BCI), which rose by 7 points to 45. This was the third consecutive increase and lifted the BCI to the highest level since early 2022. Encouragingly, the results of the Q4 business survey show that the economy has been in an upswing phase for the last two quarters. Indeed, our business cycle clock is moving closer to “Boom” territory. Of course, we still need to see a few more quarters of similar results before we get too excited but it is clear that conditions have improved in Q4 compared to a year ago and are expected to remain so next quarter.

Source: BER

The business cycle clock is derived from the unweighted average of the realised and expected business conditions of building contractors, manufacturers, retail traders, wholesale traders, and new vehicle dealers.

Finally, the SARB Monetary Policy Committee (MPC) cut the repo rate by 25bps on Thursday, following a similar reduction in September and aligning with market expectations. The decision was unanimous, with the Governor confirming that a larger cut of 50bps had not been considered. While inflation risks are currently viewed as balanced, the SARB emphasised mainly the upside potential - for example, the dollar’s strength since the US elections. For our interest rate following the meeting, clients can find a detailed Comment here. In short, the SARB will likely continue to tread carefully going forward, with many of the factors causing uncertainty unlikely to disappear over the near term. Meanwhile, the SA Revenue Service (SARS) said that it had issued more than 1.9 million tax directives with a total gross value of about R35bn. A quick sum shows that this is equal to about R18.4k per withdrawal on average. This suggests that many withdrawals are from those with pension savings of below R300k in total (as those with higher savings can withdraw R30k this year) – indicative of a consumer under pressure. SARS did not provide an update on the tax liability for these withdrawals, but it will be more than the R5bn pencilled in by the National Treasury.

Back to monetary policy, recent speeches by US Federal Reserve (Fed) officials underscore the growing uncertainty surrounding US monetary policy ahead of the December monetary policy meeting. For example, Governor Michelle Bowman, who favours a more gradual approach to easing policy, pointed to the recent stagnation in inflation, noting that headline inflation ticked up to 2.6% in October. Meanwhile, Governor Lisa Cook offered a more optimistic perspective, emphasising that inflation remains on a downward path while the labour market is gradually cooling. It appears investors were slightly more convinced by the former, and markets have started to scale back expectations for rate cuts. Last week, markets were pricing in a more than 70% likelihood of a 25bps rate cut in December; this has since dropped to 55%. The shift reflects persistent inflation, robust economic growth, and concerns over potential inflationary pressures from Donald Trump’s proposed tariffs.

In Europe, the European central bank (ECB) reported that negotiated wage growth in the Eurozone (EZ) rose sharply to 5.42% y-o-y in Q3, up from 3.54% in Q2, as workers sought compensation for incomes eroded by previous spikes in inflation. The ECB is still expected to lower its benchmark interest rate by 25bps in December. However, officials may use the wage data to temper expectations for further easing. This week, final inflation figures for the EZ confirmed a 2% y-o-y rise in October. ECB officials are also monitoring the possible inflationary impact of increased US potential tariffs expected next year.

In contrast to the Fed and ECB, which are, on balance, expected to cut in December, the Bank of England (BoE) will likely maintain its current interest rate level at the December meeting. UK inflation unexpectedly rose last month, exceeding the BoE’s 2% target. It was more concerning that headline, core, and services inflation all accelerated. Services inflation rose to 5.0% in October from 4.9% in September. Core inflation, excluding volatile components like energy and food, also edged up unexpectedly to 3.3%, compared to 3.2% in September. After its November rate cut, the BoE signalled that any future easing would be gradual, forecasting inflation to remain above its 2% target until early 2027. This projection reflects stimulus measures from the new Labour government’s first budget, including a nearly 7% increase in the minimum wage set to take effect in April. Regarding current wages, the rate of pay rises held steady in October. However, wage growth is expected to moderate next year as employers respond to higher social security contributions (mentioned in the budget) by limiting pay increases.

On the geopolitical front, we saw a significant escalation in the Russia-Ukraine conflict this week. On Wednesday, Ukraine launched British missiles at Russian territory, following a similar strike with US missiles the previous day. After reports that Ukraine had received permission to use longer-range US weapons, Russia warned that such actions would be viewed as direct involvement by Western suppliers in the war, marking a significant escalation. On Thursday, Ukraine’s air force reported that Russia retaliated with an intercontinental ballistic missile (ICBM) targeting the city of Dnipro. If confirmed, it would mark the first use of a missile designed for long-range nuclear strikes in a conventional war. However, there was no indication that the weapon was nuclear-armed and late on Thursday, two Western officials suggested that initial analysis pointed to the weapon not being an ICBM, though further investigation is ongoing.

The escalation resulted in investors seeking out safer assets this week. The US dollar reached its strongest level against the euro since October 2023. Likewise, gold benefitted, rising by 3.8%. Brent crude oil prices also rose amid the threats of war, particularly the potential involvement of two of the biggest oil producers in the world, namely Russia and the US. However, the rand bucked the trend, gaining against the dollar, euro and pound. Further still, the JSE Alsi rose by 1.3%. Among global bourses, the US’s S&P 500, Germany’s DAX and Japan’s Nikkei all posted losses. However, after a strong Thursday, the UK’s FTSE 100 was up this week.

In the EZ, key sentiment indicators from Germany will take centre stage. Business sentiment for October and consumer sentiment for November showed improvement, but slight declines are anticipated in the upcoming releases. Germany’s economy has had a torrid year, with its manufacturing sector, particularly auto manufacturing, under significant strain. After Volkswagen recently warned of potential plant closures in Germany for the first time in 87 years, Ford has followed suit. The auto manufacturer announced plans to cut 4 000 jobs across Europe, with the majority in Germany. Although these cuts, affecting 2 900 German workers, are expected to be implemented gradually through 2027 and represent a small fraction of the national workforce, they signal further challenges for the sector. Companies have cited weak demand for (high-cost) electric vehicles (EVs), insufficient government support, and competition from cheaper Chinese EVs as key constraints. Compounding concerns, Germany faces potential economic fallout if incoming US President Trump implements a proposed 20% blanket tariff.

Staying in the EZ, preliminary consumer inflation data for November is due on Friday. While a slight uptick in inflation is expected, it is unlikely to deter the ECB from delivering a modest rate cut in December.

In the US, the Fed will release the minutes from its November meeting, during which the FOMC opted for a 25bps rate cut. Key US data releases include October’s Personal Consumption Expenditures (PCE) price index and the second estimate of third-quarter GDP growth. The latter is unlikely to differ from the initial estimate of 2.8% q-o-q annualised growth.

Turning to SA, the SARB will release the leading business cycle indicator for September. Following a monthly decline in August, expectations point to a modest improvement. Additionally, private credit extension figures will be released on Friday. In addition, Stats SA is set to publish October’s Producer Price Index (PPI) on Thursday. September’s increase of just 1% was the lowest since 2020, with producer price pressures likely to remain subdued.

The RMB/BER Business Confidence Index (BCI) rose by 7 index points to 45 in 2024Q4, with a broad-based improvement across different business sectors. This means that 45% of the respondents were satisfied with prevailing business conditions. Underpinning the improved sentiment was an increase in activity and better business conditions. Encouragingly, business conditions are expected to improve further in the next quarter, and this bodes well for business sentiment. In a further positive development, the indices tracking purchasing and selling prices declined in Q4, signalling some relief in price pressures. This trend is likely to be welcomed by the SARB, as it aligns with efforts to stabilise consumer inflation at the 4.5% midpoint of the target range. See the BCI press release here for more detail.

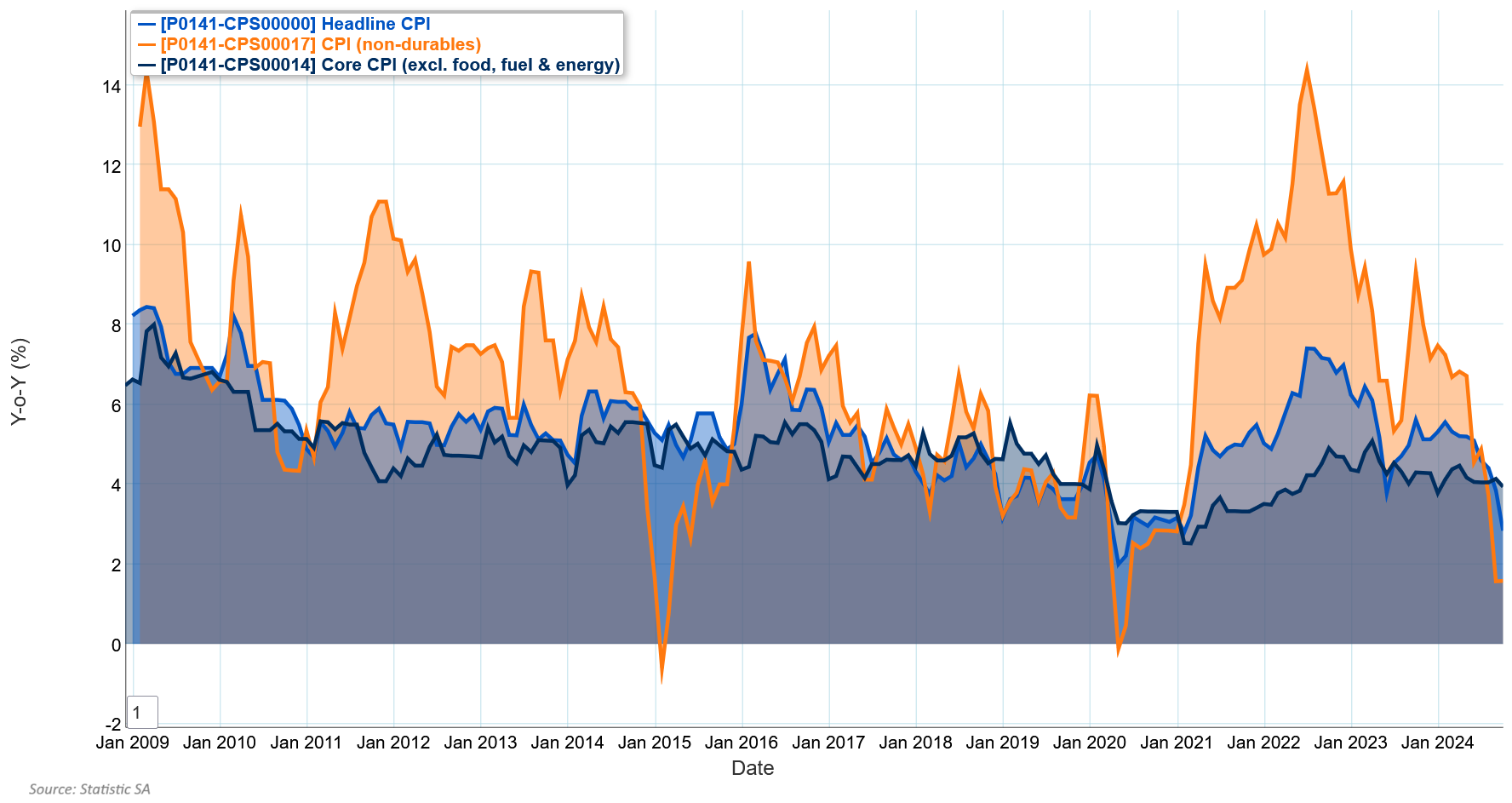

Headline consumer inflation (CPI), as reported by Stats SA, moderated significantly to 2.8% y-o-y in October, down from 3.8% y-o-y in September. This was driven primarily by a sharp decline in transport inflation, with transport prices dropping by 5.3% y-o-y and 1.5% m-o-m, largely due to falling fuel prices. Other key categories showed notable moderation, including food and non-alcoholic beverages (up 3.6% y-o-y compared to 4.7% in September) and restaurants & hotels (up 5.9% y-o-y vs 7.4%). Core inflation, which excludes volatile food and energy prices, edged down by 0.2% pts to 3.9% y-o-y, after holding steady at 4.1% for two consecutive months. This suggests that persistent inflationary pressures are easing.

Members of the SARB's Monetary Policy Committee unanimously decided to cut the repo rate by 25 bps, reducing the policy rate to 7.75%. As in September, the SARB continues to view inflation risks as broadly balanced. On the growth front, the SARB maintained its 2024 GDP growth projection at 1.1% but revised its 2025 forecast upward to 1.8%. The improved outlook for 2025 is underpinned by factors such as lower inflation, rising real incomes, and additional consumer spending driven by two-pot pension withdrawals.

Stats SA released a slew of internal trade data this week, revealing mixed results across trade sectors. In the retail sector, real sales grew by 0.9% y-o-y in September, following an upwardly revised 3.3% increase in August. General dealers were the strongest performers, with sales rising by 4.5% y-o-y and contributing 2.1% pts to the overall figure. Meanwhile, retailers in textiles, clothing, footwear, and leather goods reported a 5.5% decline, subtracting 0.9% pts from the overall figure. On a monthly basis, seasonally adjusted (sa) retail sales declined by 0.8% in September, after a 0.6% increase in August. Despite this monthly dip, sales expanded by 0.7% q-o-q – positive for Q3 GDP dynamics.

Wholesale trade, however, continued its downward trend, with real sales contracting by 6.5% y-o-y in September, following an 11.2% drop in August. This extended the sector's losing streak to 13 consecutive months. On a monthly basis, wholesale trade sales (sa) rose by 1.1% in September, recovering partially from a 2.3% decline in August. Indeed, this monthly rebound was insufficient to offset earlier losses, resulting in a 2.9% q-o-q contraction in Q3.

Motor trade also fared poorly, with real sales falling by 7.1% y-o-y in September after a 3.9% decline in August. The drop was largely driven by weaker demand for new vehicles, which plunged by 13.9% y-o-y, as financially constrained consumers shifted toward more affordable used vehicles, which saw a 5.6% y-o-y increase.

UK headline consumer inflation in the UK accelerated to 2.3% y-o-y in October, up from 1.7% in the previous month. This was higher than the 2.2% expected by the Bank of England (BoE). The main drivers behind this acceleration were electricity and gas prices. Electricity prices declined by ‘just’ 6.3% y-o-y, compared to a 19.5% decline in the previous month, while gas prices fell by 7.3% y-o-y versus 22.8% the month before. This was primarily due to Ofgem, the UK's energy regulator, increasing the cap on electricity and gas prices in the fourth quarter. The cap, which limits the maximum amount energy suppliers can charge per unit, was lifted by 10% from previous levels. At the same time, services inflation also accelerated from 4.9% y-o-y in September to 5% in October, largely in line with the BoE forecast.

Looking ahead, there are upside risks to inflation in the UK stemming from policies announced in the October budget speech. These measures include an increase in national health insurance contributions, a rise in the cap on single bus fares from £2 to £3, the introduction of VAT on private school fees from January, and an increase in Vehicle Excise Duty from April. Given these upside risks to inflation, investors are only fully pricing in the next 25 bps cut in March, with a lower probability for a cut in December.

Similarly, a final estimate confirmed that EZ consumer inflation reaccelerated in October compared to the previous month. Eurostat reported that inflation picked up to 2% in October from 1.7% in September. Even though this aligns with their inflation target, the underlying drivers for the reacceleration are worrying. Food, alcohol, and tobacco inflation reached 2.9% in October, up from 2.4% in September. The offsetting effect from lower energy prices was also less pronounced in October, with energy prices declining by 4.6% compared to a 6.1% decline the month before.

Services inflation, meanwhile, rose from 3.9% in September to 4% in October. Although it has followed a generally downward trajectory, the latest annual increase in negotiated wages does not bode well for the continuation of the disinflationary path. Negotiated wages in the Eurozone increased by 5.42% in 2024Q3, up from 3.54% in the second quarter—the highest reading since 1993Q1. Germany was the main culprit behind the higher negotiated wage growth. While the ECB expects wage growth to slow down, if Germany continues to drive the regional trend, it may limit the scope for further rate cuts.

Meanwhile, preliminary survey results from the European Commission showed that EZ consumer sentiment deteriorated by more than expected in November and fell to its lowest level in five months.

We recently launched the beta version of the BER Data Playground. To showcase the data freely available on the Playground, we will regularly publish a chart in the Weekly. Today we focus on the data published by Stats SA earlier this week.

In October, headline inflation came in below expectations at 2.8%, marking a significant milestone in price stability efforts. Core CPI, which excludes volatile categories such as food, fuel, and energy, remained relatively sticky at 3.9%, a negligible decline from 4.1% previously. Meanwhile, inflation for non-durables declined from 3.5% to 1.2%, the lowest level recorded since May 2020.

Editor: Lisette IJssel de Schepper

Email: lisette@sun.ac.za

Click here for previous editions of this publication.

Please refer to the glossary on the BER website for explanations of technical terms.

Friday, 22 Nov 2024