General

Publications & Data

Join the conversation

Social Links

Social Links

It was a busy week on the domestic economic data calendar, but unfortunately there was little encouraging news about the state of the SA economy. Real GDP eked out a slight expansion in 2023Q4 and thereby managed to avoid slipping into a technical recession, but according to the RMB/BER Business Confidence Index (BCI), business conditions remained bleak in 2024Q1. On the global front, the European Central Bank (ECB) had its second policy meeting of the year. As expected, the central bank kept the interest rate unchanged, but signalled that a June rate cut might be on the cards, pending upcoming wage data. In the same vein, US Federal Reserve (Fed) chair Jerome Powell emphasised during his congressional testimony that it was not ready to cut rates (its next meeting is in two weeks), but hinted that cuts would come later this year. The other big announcement over the week was the Chinese growth target and other economic targets for 2024.

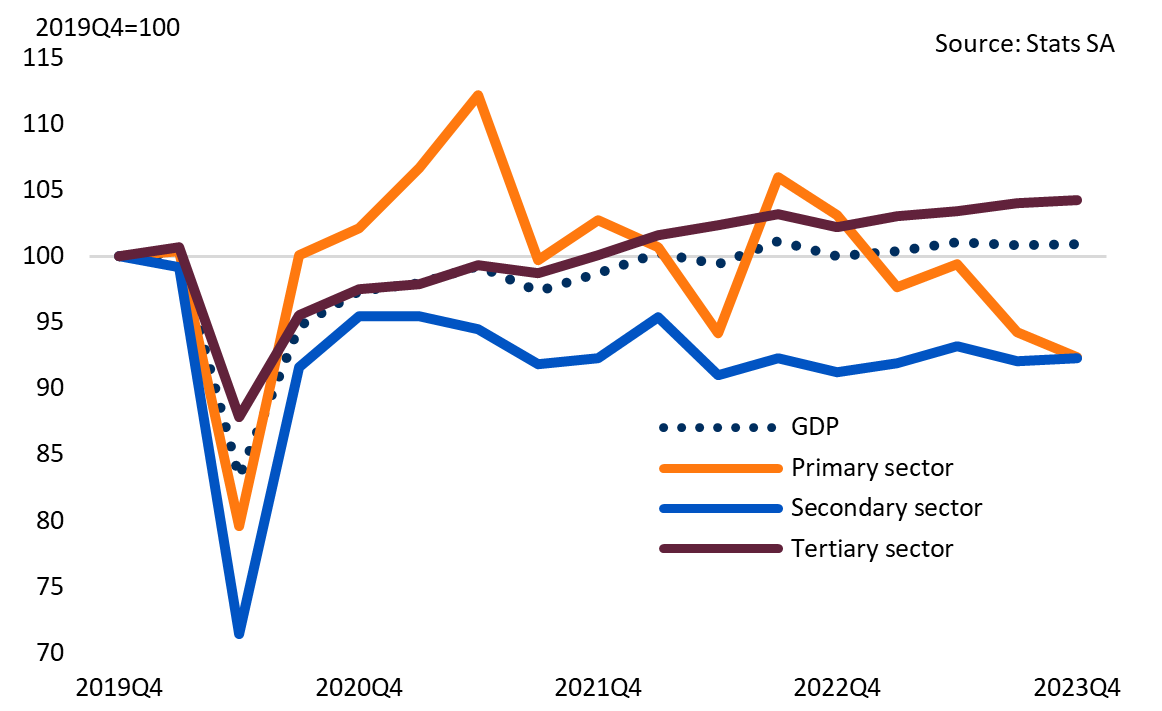

Starting with the domestic developments first, much was made of the SA economy ‘escaping’ a technical recession (i.e. avoiding two consecutive quarters of declining quarterly GDP growth). While true, this does not take away from the fact that the GDP data was poor. The economy grew by a mere 0.6% in 2023. Taking a slightly longer-term perspective, it is depressing to note that the economy is barely 1% larger than it was in pre-pandemic 2019Q4. From the production side, the post-pandemic recovery has been driven by growth in the tertiary (services) sector. Indeed, on the back of a very poor (and volatile) performance by the agriculture sector in recent quarters, the primary sector has now dwindled lower once more. The secondary sector (mainly manufacturing and construction) has moved sideways over the last three years without ever recovering to pre-COVID levels. On the expenditure side, investment is the biggest drag on growth, and lost further momentum in 2023Q4 - clients can click here for more on GDP. Worryingly, the RMB/BER BCI for Q1 suggests that sentiment among businesspeople in the SA economy remained very poor. This means that non-energy investment is set to remain lacklustre.

Also underwhelming (but just as impactful as the performance of the Chinese economy) was the confirmation that a rematch between current US President Joe Biden and former President Donald Trump seems all but set following Super Tuesday. After dominating the primary elections on Tuesday, both Biden and Trump are very close to securing their party’s nominations. On the Republican side, Nikki Haley dropped out of the race on Wednesday with some analysts quipping that the only Republican candidate that Trump has left to compete with is himself. Biden delivered a feisty state of the union speech yesterday, making his case for re-election.

In commodity markets, the gold price stole the show with the yellow metal reaching record highs once more. The price was up by more than 5% (or more than $100/oz) from last Thursday. This could be due to somewhat softer data from the US leading markets to increase the likelihood of a rate cut by the US Federal Reserve in June (lower rates are positive for the gold price) – US bond yields also ticked down. However, there is likely also some speculative trading at play. The gold price has been on a tear since early 2022, initially due to increased buying from emerging market central banks following the Russian invasion of Ukraine, but now also from Chinese buyers as their local property and stock market take strain. The sustained surge has been despite high global interest rates.

The other big story in commodity markets was the decision by OPEC+ members to extend their voluntary production cuts to the end of June. The series of cuts since late 2022 are now equal to about 5% of global oil supply, with Saudi Arabia bearing the brunt. Non-OPEC members (mostly the US and Canada) have steadily filled up the gap. Indeed, the Brent crude price moved only slightly higher and was up by just 0.4% w-o-w.

The rand clawed back most of its recent losses and closed Thursday firmly below R19/$. While the dollar was generally weaker and this helped the rand, the local currency also appreciated against the euro and pound. The JSE ALSI was up by 1.2% since Thursday. US markets rose yesterday following Powell’s speech that suggested rate cuts are imminent.

Finally, it is worth mentioning the developments in Egypt over the past week. Following “decisive steps to move towards a credible flexible exchange rate regime” and a 600bps increase in their policy interest rate (on top of an earlier 200bps hike), the country essentially secured a deal to more than double its IMF bailout (from $3bn in 2022 to $8bn). Egypt has been reluctant to let its currency depreciate as it was worried about the inflationary impact, with inflation running close to 30% already. The changes have been made possible by a $35bn injection by ADQ, an investment vehicle from the United Arab Emirates. The flexible exchange rate will be beneficial over the long term, but fiscal discipline going forward will be important to stave off further pain.

Stats SA will release mining and manufacturing production data for January, providing an initial glimpse into Q1 GDP dynamics. Worryingly (although not unexpected), this week’s electricity production fell by 1.7% m-o-m in January as load-shedding was more intense compared to December. This, and continued issues at local rail and ports, are also set to have weighed on industrial production in January. The Absa PMI suggests that the manufacturing sector experienced a very poor start to the year, meaning it could see another monthly drop. Mining production fell by a steep 4.2% m-o-m in December as iron ore production slumped by 28.6%. This was due to a big miner cutting back output to prevent stocks from running too high with exports due to port congestion – this is unlikely to have changed in January, but another m-o-m drop of that magnitude is unlikely.

Next week is relatively quiet on the international front, with the most keenly watched release coming on Tuesday: US inflation. This is especially true because of the Fed policy rate meeting the week after. Although to be sure, markets may adjust their expectations about the probabilities of cuts coming in later months, even a sharp downward surprise in February inflation is not going to put a March rate cut (back) on the table. Indeed, headline inflation is not expected to slow down from January’s 3.1% y-o-y, but core inflation could tick down somewhat from 3.9%. Later today sees the nonfarm payrolls data for the US, which like the inflation print next week, could result in some market volatility if it surprises consensus.

According to Stats SA, real GDP registered a mere 0.1% q-o-q growth in 2023Q4 following a contraction of 0.2% in Q3. As such, economic growth averaged 0.6% in 2023 from 1.9% in 2022, in line with our expectations. While the economy escaped a technical recession in Q4, the performance remains uninspiring. From the production side, the transport industry made the biggest positive contribution to quarterly growth (0.2%pts). Adversely, the domestic trade sector shaved 0.3%pts off GDP growth, while agriculture surprised on the downside again (-0.2%pts). On the expenditure side, government consumption and inventories did better than expected, boosting GDP, while lower investments and higher-than-anticipated imports weighed on GDP growth. Net trade shaved 1%pts off growth as imports rose by 2.4%, while exports increased by only 0.6%.

Clients can click here for a detailed comment on the GDP release.

In step with the poor trade data from the GDP release, the SA Reserve Bank’s (SARB’s) current account release for 2023Q4 highlighted a shrinking trade surplus. The trade surplus decreased from R181.1bn in Q3 to R88.1bn in 2023Q4. This decline occurred due to the pace and cost of imports outstripping those of exports. Looking at the year as a whole, the trade surplus declined to 1.5% of GDP in 2024 from 3.4% in the previous year.

The smaller trade surplus and a wider deficit in services, income and transfers meant that the current account deficit increased from 0.5% of GDP in Q3 to 2.3% of GDP in Q4 – this was a worse outcome than the consensus forecast had anticipated. For the full year, the deficit widened to 1.6% of GDP from 0.5% of GDP in 2022.

The S&P Global SA PMI increased to 50.8 in February from 49.2 in January. Broadly speaking, the results are in line with last week’s Absa PMI (click here for the full report). Respondents highlighted supply-side challenges as a major impediment to activity, which still contracted – albeit at a slower rate. The situation at the Durban port continues to stifle operations, while delivery times lengthened, and some firms report increased delivery and transportation fees. The logistics crisis also severely affected exports, marking the seventh consecutive month of declines, which offers one explanation for the weaker export trade on the current account.

On a positive note, employment and inventories grew in February. In line with these numbers, respondents were also more optimistic about business volumes over the next 12 months. The S&P PMI results also showed relatively subdued price increases, which is promising for our expectations of softer producer price inflation in the first quarter of 2024.

Following a two-point decline in the fourth quarter of 2023, the RMB/BER Business Confidence Index (BCI) ticked down by another point to reach 30 in the first quarter of 2024. This means seven out of ten survey respondents are unsatisfied with prevailing business conditions. A slightly longer perspective shows a concerning picture, as less than four out of ten survey respondents were satisfied with prevailing business conditions over the last seven quarters.

Broadly speaking, business activity remained poor while business conditions deteriorated further. As in the fourth quarter of 2023, this result went against survey respondents’ expectations for an improvement. Remarks about the negative impact of load-shedding, the state of the local ports, crime, and political uncertainty featured prominently in the feedback from survey participants.

Worrying for Q1 GDP dynamics, both the PMIs and BCI composite activity index suggest a marginal decline in activity for the first quarter of 2024.

SA’s foreign exchange (forex) reserves increased to US$61.7bn in February from US$61.2bn in January, above the market expectations of US$61bn. The increase comes mainly from a stronger dollar trading on average at R19.20 in February compared to R18.74 in January. In contrast, there was a decrease in gold reserves (US$8.18bn in February from US$8.22bn in January), reflecting the slight monthly decline in the gold price (-0.5%).

As widely expected, the ECB kept its key policy rate unchanged at a record high. Acknowledging that inflation has slowed further since the previous meeting, the central bank has downwardly revised its inflation and growth projections. The latest ECB staff projections now see annual headline inflation average 2.3% in 2024 (from 2.7% in December), while growth has been revised down to 0.6% in 2024 from 0.8%. The ECB remains attentive to the upside inflation risks posed by geopolitical uncertainties and robust wage growth – particularly in the services sector. The latter has been highlighted by last week Friday’s release of the EZ’s inflation print, which showed that owing to persistently high service inflation, both headline and core CPI eased less than expected in February. In a press conference on Thursday, ECB President Christine Lagarde stressed that the central bank is “particularly vigilant about wages and profits”. Therefore, we are likely to only see a shift in the ECB’s hawkish tone following wage settlement data in May, with a cut possible in June.

Moving to the US, the ISM Services PMI fell to a below-consensus 52.6 in February, down from a four-month high of 53.4 in January. The latest reading marked a fourteenth consecutive month of expansion in service sector activity, albeit at a slightly slower pace. The decline was due to supplier deliveries moving from 52.4 in the previous month to 48.9 and the employment subindex declining from 50.5 to 48 in February, entering contractionary territory. However, respondents remain optimistic about business conditions as business activity and new orders expanded at a faster pace. Meanwhile, price pressures eased from 64 to 58.6 in February, which is a somewhat encouraging indication of US inflation developments.

Lastly, China’s trade surplus increased to $125.2bn in January and February, beating market expectations of a $103.7bn surplus. Exports rose by 7.1% y-o-y, surpassing expectations of a 1.9% increase. This was largely driven by growing exports of mechanical and electronic products, accounting for almost 60% of exports. Meanwhile, imports grew by a softer 3.5% y-o-y but still beat the consensus forecast of a 1.5% rise.

Editor: Lisette IJssel de Schepper

Tel: +27 (21) 808 9777

Email: lisette@sun.ac.za

Click here for previous editions of this publication.

Please refer to the glossary on the BER website for explanations of technical terms.

Friday, 08 Mar 2024