General

Publications & Data

Join the conversation

Social Links

Social Links

By: Lisette IJssel de Schepper

This week's big event was the Budget Review presented by the National Treasury (NT) on Wednesday. The key announcement was the confirmation that NT would be drawing down on the SA Reserve Bank’s (SARB’s) Gold and Foreign Exchange Contingency Reserve Account (GFECRA). A detailed comment was released to clients on Wednesday (click here), but we briefly summarise the most important budget announcements below. This week also saw local inflation data for January, which reflected a slight acceleration from December on the back of higher fuel prices. Meanwhile, total employment edged down slightly q-o-q in Q4, which, coupled with an uptick in people looking for work, meant that the unemployment rate increased.

On the international front, the February flash PMI figures for Europe and the US were released. In the US, both services and manufacturing performed well, while across the Atlantic, the services sector is doing better than factory activity. China announced further stimulus, while US Federal Reserve (Fed) policymakers indicated that they would rather cut the policy rate too late than too soon.

Coming back to the GFECRA. The technical details fall outside of the scope of the Weekly, but we do want to highlight that using these funds per se is not against global best practice. NT will receive a net R100bn in 2024/25, with further drawdowns of R25bn each in the next two fiscal years. Another R100bn will flow back to the SARB, which means that the total drawdown is R250bn (or roughly half), still leaving a sufficiently big buffer in place. If managed prudently and spent wisely, these funds can make a meaningful contribution to alleviating some pressure on the SA fiscus. Indeed, the better debt-to-GDP and deficit projections over the medium term are largely due to utilising the GFECRA funds. It is, however, not a long-term solution to the structural ailments facing the SA economy – it merely buys SA some time to generate faster economic growth. The February budget means that NT now sees debt-to-GDP peak at 75.3% of GDP in 2025/26, from 77.7% before (November). This still only moves down very slowly, with the shape of the trajectory largely unchanged.

While we still have to crunch the numbers now that we have some (although not all) details on the amount and timing of the GFECRA drawdown, we are likely to remain more downbeat on the debt-to-GDP ratio than NT (although we will likely end with a lower number than the 83% peak we had pencilled in for 2027/28). On the near-term deficit view, NT does not bring Eskom transfers in when calculating the deficit. This also means that their primary budget surplus1 of 0.3% of GDP in the last fiscal year is a bit misleading. This is important to note because in the absence of a formal new fiscal anchor (which needs to be legislated), NT is using achieving primary budget surpluses as their goal – but this only happens much later than their current estimates when you take full account of the Eskom transfers.

As expected, NT stayed clear of ‘electioneering’, although the absence of a fuel levy increase and references to the National Health Insurance in the speech were perhaps glimmers of that. Tax rates were not increased, but bracket creep (not adjusting the personal income tax brackets for inflation) will put additional pressure on the already struggling (tax-paying) consumer. Increases in grants, in turn, will help. NT remained stern on providing further support to State-Owned Enterprises (SOEs) – with Transnet conspicuous in its absence.

The initial market reaction to the Budget was positive. Bond yields declined and the rand strengthened. However, yesterday afternoon the rand started to slide. The currency has since reversed all gains made on Wednesday and is, in fact, more than 1% weaker to the dollar, pound and euro since last week Thursday. The JSE ALSI ticked up by just over 1% w-o-w, with the global performance mixed. The standout last week was the Japanese stock market which reached a record-high level. This was mainly on the back of chip-related shares. In the US, solid corporate results boosted the share price of chipmaker Nvidia, benefitting the broader market.

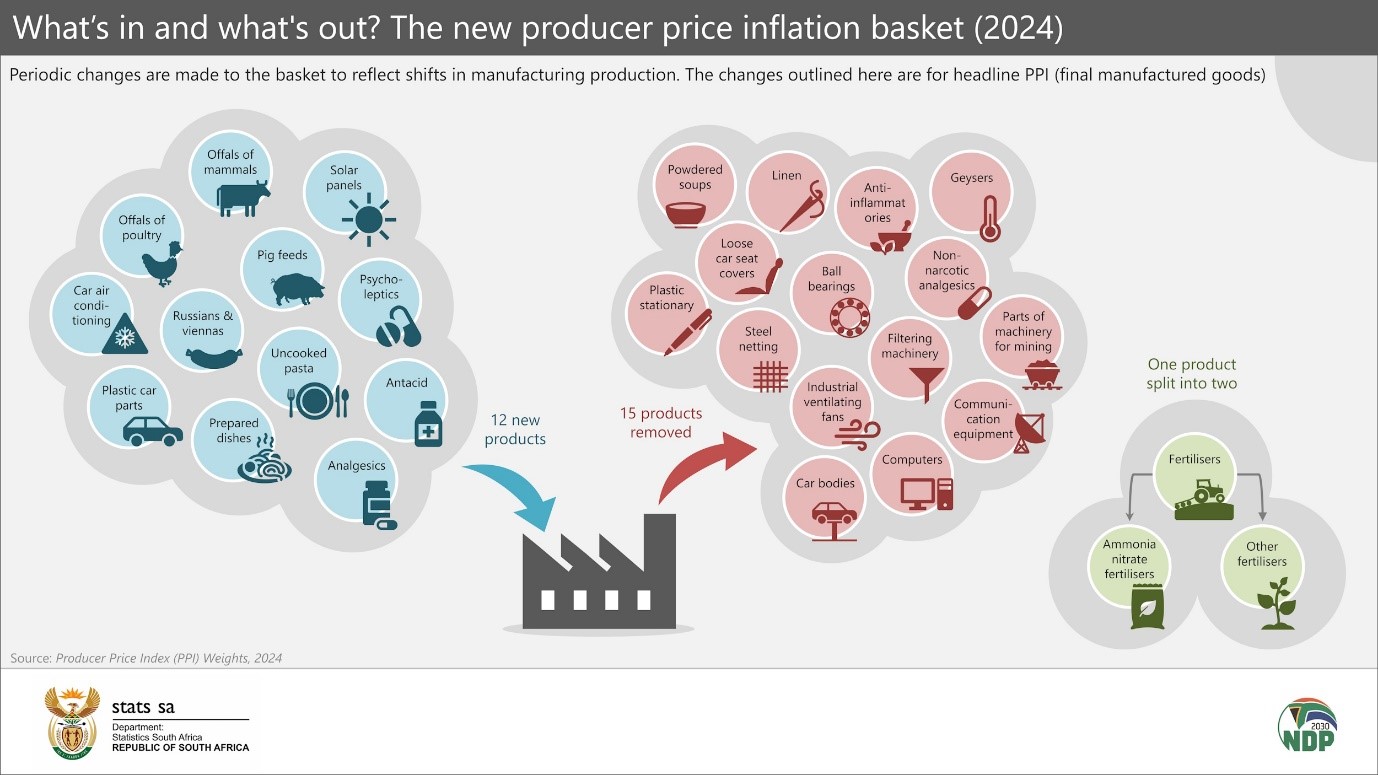

The most important SA data releases come late in the week. Thursday sees private sector credit data as well as the producer price inflation (PPI) print, both for January. The January PPI will be the first release based on a reweighted basket – see this infographic from Stats SA for some of the changes in the goods included in the calculation for final manufactured goods. While the changes complicate the forecast slightly, we expect January PPI, like CPI, to reaccelerate slightly at the beginning of the year on the back of higher fuel prices. The trade balance for January will also be released on Thursday.

On the international front, the markets keenly await the Fed’s preferred measure of inflation for January released on Thursday. Any surprises may result in another readjustment in the expectations of the timing of the first interest rate cut – the same goes for the second estimate of US GDP growth for Q4. The Chinese PMI figures (out early on Friday, so before the release of the next Weekly) will give an important update on the strength of the Chinese economy.

1The primary balance is the difference between total revenue and non-interest expenditure, and is a key driver of government’s debt stock. In general, when the primary balance is in deficit, the debt-to-GDP ratio can be expected to rise. When the primary balance is in surplus, the debt-to-GDP ratio can be expected to fall.

By: Romano Harold

After two consecutive months of moderation, headline CPI accelerated to 5.3% y-o-y in January from 5.1% y-o-y in December, data from Stats SA showed. The headline reading was in line with our expectations. As expected, a big driver of the increases was an acceleration in transport costs, up to 4.6% y-o-y in January from 2.6% y-o-y in December. However, for the second consecutive month, inflation for food and non-alcoholic beverages eased (up ‘only’ 7.2% y-o-y vs 8.5% y-o-y). Headline CPI increased by 0.1% m-o-m in January after a fat reading in December. Meanwhile, core inflation, which excludes food and energy costs, unexpectedly accelerated, rising to 4.6% y-o-y, a five-month high, from 4.5% y-o-y in December.

According to the Quarterly Labour Force Survey (QLFS), the official unemployment rate increased to 32.1% in 2023Q4 from 31.9% in Q3. The latest print was a touch higher than the Bloomberg market consensus for an improvement to 31.6%, marking the end of a year-long decline in the headline rate. The rise in unemployment was due to 46 000 individuals joining the ranks of the unemployed, while the number of employed persons declined by 22 000. Job losses were broad-based, with the community and social services sector hardest hit, shedding 171 000 jobs. In contrast, the finance sector reported the largest job gains (+128 000).

Finally, according to data from the SARB, the composite leading business cycle indicator (LEI) continued a streak of declines. In December, the LEI fell by 0.8% m-o-m, the most since May, following a 0.4% m-o-m drop in November. While five of the nine component time series increased, this was marginally outweighed by declines in the four remaining components. The main negative factors were decreases in approved residential building plans and the average hours worked per factory worker in the manufacturing sector. On a more positive note, there were accelerations in the six-month smoothed growth rate of new passenger vehicles sold and in job advertisement space.

By: Nicolaas van der Wath

Regarding the Eurozone’s (EZ) real economy, the flash HCOB Composite PMI rose from 47.9 index points in January to 48.9 points in February, the highest in eight months. However, the reading remains below the neutral-50 level and does not point to growth. The increase was bolstered by a rise in the PMI of the services sector to 50 points, while the manufacturing PMI declined to 46.1 points. Of concern is that both purchasing and selling prices increased slightly faster than in January. If inflation remains sticky above the target, interest rates may need to remain constrictive for longer. Annual consumer inflation for January was confirmed at 2.8%. Although EZ Core inflation continued to slow, at 3.3%, still remains above the target and headline number. This week sees the flash estimate for February CPI.

In the UK, the composite PMI reached a more upbeat 53.3 index points. Like in the EZ, this was mostly the services sector where activity levels increased as the manufacturing index remained in contractionary territory (47.1). Price pressure remained elevated, especially due to higher wages in the services sector.

Meanwhile, in the US, the S&P Global Composite PMI dipped to 51.4 – a two-month low as services fell, but manufacturing moved higher. Both sectors continued to record growth in output, suggesting that the economic outperformance of the US relative to Europe continues.

Regarding monetary policy in the US, the minutes of the January meeting of the Federal Open Market Committee (FOMC) were released. Members felt that the policy interest rate is probably at its peak of the current tightening cycle, but need more convincing evidence that inflation is anchored at its target before rates can be reduced.

Finally, in an effort to support the struggling property sector, the People’s Bank of China (PBoC) lowered its five-year prime lending rate (for mortgages) by 25 basis points. The rate is now at 3.95%, the lowest since it was introduced in 2019. The reduction was also the largest since then. The reduction follows a large liquidity injection and a relaxation of reserve requirements earlier in the month.

Lisette IJssel de Schepper

Tel: +27 (21) 808 9777

Email: lisette@sun.ac.za

Friday, 23 Feb 2024

{kind=link}